2016年3月6月ACCA P3考试真题及答案

-

The country of Westoria has a well-respected public health service funded primarily through general taxation. The Westoria Public Health Authority (WPHA) is responsible for delivering this health service through a network of hospitals in Westoria.

WPHA is under increasing pressure to demonstrate to taxpayers that it is using public finances wisely and so it wishes to accurately monitor and control health service expenditure. However, it is proving difficult to confidently track the budgeted and actual finances of individual hospitals, as each is operating its own form. of budgeting and cash management. Consequently, WPHA has decided to introduce a single computer-based system which will allow all hospitals to enter and manage financial information in a standard way. This system will be part of an authority-wide enterprise resource planning system (ERPS) which will allow WPHA to monitor and control the finances of the entire authority. Currently, the input and consolidation of WPHA information is a time-consuming process, importing data from individual hospitals into a series of spreadsheets to provide total figures for the authority as a whole.

At a recent WPHA board meeting, the head of the authority suggested that the scope of the ERPS should be widened to incorporate other elements of operational and management information. She pointed out that some previous commercial off-the-shelf (COTS) software solutions which the authority selected and implemented had not worked well. She gave two specific examples:

– The payroll system does not support payment increments for non-standard working, such as overtime rates. To allow this, payroll staff currently have to change the employee’s standard hourly rate for the time period in question and then change it back again. This is time-consuming and payment errors have been made when payroll staff have forgotten to change the rate back again.

– The human resource management system does not support the temporary transfer of staff between hospital departments. To compensate for this, human resource staff have to action a permanent move for a short time period and then action a reverse move at the end of that period.

She therefore felt that the introduction of the ERPS would be an opportunity to address outstanding problems and to improve and standardise the systems in use.

The board agreed the ERPS should, as a minimum, also include payroll and human resource management modules within the overall product. However, given budget limitations, the board decided that a commercial off-the-shelf ERPS solution should be selected and implemented. They all agreed that this would be a cheaper solution than a bespoke system and would be well suited to their needs, as it should fulfil the standard requirements they envisaged. Furthermore, it had always been the policy of WPHA not to employ internal IT system developers. Currently, the IT support team consists of one operational member of staff at each hospital and a central team of ten staff who assist in addressing major IT problems encountered at any of the hospitals. The IT support team has also produced ways to bypass issues with previously implemented COTS package solutions.

This lack of internal IT resource, and the recognition that previous COTS implementations had been less successful than predicted, has prompted WPHA to seek the advice of an external software systems consultant.

The consultant has suggested that the evaluation and implementation of the ERPS package should follow a four-stage process:

– Evaluate whether a COTS solution is an appropriate approach

– Define the requirements for the new software

– Evaluate competing packages

– Implement the selected package

However, the head of the authority believes that the external consultant is being over-cautious in his advice and approach and that the first two stages are not needed. In her words: ‘We know that a COTS solution is the right approach for us as we have little alternative, so why spend time doing the first step? We also know that we’ve been pretty poor at defining what we want in the past; so why not recognise our deficiencies and go straight to stage three and look at competing packages to see which products provide the best features?’

The HR director, who has experienced the problems of the human resource and payroll systems at first hand, disagrees. He feels that the consultant’s four-stage process is insufficient. He believes that, ‘it is important that we consider all four elements of the POPIT (four view) model, which provides four key areas to be considered when a process is to change. These four key areas are people, organisation, processes and information technology. Only the last of these will be considered in the consultant’s four-stage process. If we ignore the remaining three areas we are in danger of another failed software project, which is likely to further upset taxpayers and, perhaps, threaten the future of the authority itself.’

Required:

(a) The external consultant suggested a four-stage process for the evaluation and implementation of the proposed commercial off-the-shelf ERPS package.

Discuss the four-stage process for the evaluation and implementation of a software package, and the significance of each stage in the context of the previous and proposed COTS solutions at WPHA. (16 marks)

(b) The HR director has suggested that all elements of the POPIT model should be considered.

Explain, in the context of WPHA, the need for considering the people, the organisation and the processes involved when carrying out a business change project. (9 marks)

-

Section B – TWO questions ONLY to be attempted

Shop Reviewers Online (SRO) was founded in 2010 by Amy Needham. She felt that many customers buying from online stores were misled by advertising and that too often, purchased products turned out to be unreliable, faulty or failed to meet the customers’ expectations. Amy believed that the online retail industry was increasingly acting unethically, caring only for profits at the expense of the needs and expectations of customers.

Consequently, she set up SRO to ‘provide an unbiased review of online stores to ensure the customer has all available information’. The company offers reviews of current online stores and provides direct links for customers to shop at the stores featured on its site. The reviews include price comparisons, provided by SRO, as well as general reviews provided by registered users of the site. The company has two main revenue streams. The first is advertising revenue from online stores who place advertisements on the SRO site. The second revenue stream is commission from sales by online stores to customers who have clicked on the sponsored links provided on the SRO website. This commission is only paid by stores who have entered into such a commission arrangement with SRO.

SRO relies upon its website being available online 24 hours a day, 7 days a week. For this reason it has backup servers running concurrently with the main servers on which data is processed and stored. The servers are directly linked so that any update to the main servers automatically occurs on the backup. The servers are all housed in the same computer centre in the company head office. The computer centre has enhanced its security by implementing a fingerprint recognition system for controlling access to the site. However, as the majority of staff at headquarters are IT personnel, and often temporary staff are hired to cover absentees, the fingerprint recognition system is not comprehensive and, to save time, is often bypassed. Similarly, to save time needed to set up new permanent staff with passwords to access the company’s systems, a general ‘administrator’ user has been created, with the password ‘password’. Many temporary staff access the system in this way.

SRO has an intelligent software application which constantly searches the internet for product price changes, uploading these into the reviews of the online store in question. Sometimes, however, there have been problems. Usually this is when the application has not recognised an outdated page and has replaced the correct latest price with an old price found on the outdated page. Furthermore, this intelligent software application needs permanent continual access to the internet, and SRO has identified a problem with its firewall which has prevented the software application from sometimes updating the internal systems. For this reason, it has removed the firewall protection to help ensure that the correct up-to-date prices of all online stores are shown on the website.

SRO rarely generates other elements of reviews (such as product experience), leaving this to registered users of the site. However, it will, occasionally, submit its own review to help boost a store which pays a higher commission rate than its competitors. SRO is always honest in its reviews, but the more reviews a store has, the higher up the search list it appears, when a customer searches for a specific product.

Registered users can submit as many reviews as they wish. Unregistered users may also submit reviews, which will be published under the name ‘anonymous’, but these reviewers will be unable to comment on the reviews of others. SRO checks reviews for appropriate content, but does not contact the store to verify the accuracy of the review.

SRO is about to undertake an audit of the adequacy of its general and application IT controls. In addition, SRO is currently undertaking an internal ethical governance audit, which has identified two main areas of concern:

(1) Commercial conflicts of interest

As mentioned earlier, SRO’s business objective is to ‘provide an unbiased review of online stores to ensure the customer has all available information’. However, the audit has revealed that both SRO’s revenue streams may cause an ethical dilemma with regards to this objective.

(2) Company offices

SRO has little need for traditional offices, as it does not have a direct customer-facing role. It mainly requires IT technicians to support its automated services. The company has carried out research which suggests that the IT skills it requires could be sourced at a much lower rate overseas. It is considering relocation to one such country. This country has low rates of corporation tax and cheaper labour costs. However, the country itself is poorly regulated and does not have legislation concerning the quality of information systems or the security of data contained within them, particularly relating to personal data. The culture of the country is such that accepting unauthorised payments for services is also not unusual. Whilst SRO does not condone this in its code of conduct, it is aware that such issues exist in the country under consideration.

Required:

(a) Evaluate the adequacy of the general and application controls in place within SRO, with respect to its information technology and information systems. Suggest any improvements you consider to be necessary. (15 marks)

(b) Assess the corporate governance and ethical dilemmas identified by SRO in its possible relocation to the foreign country and discuss the implications of these on organisational mission, purpose and strategy. (10 marks)

-

The Holiday Company (HC) currently offers travel agency services by giving travel advice and making travel bookings for customers who physically visit the offices located in most major towns in the country. However, it is progressively reducing this part of the business while simultaneously trying to achieve a greater proportion of its revenue online.

To help meet this objective, HC is in the process of forming a new business unit to market and sell luxury holidays. The holiday product range marketed by this new business unit will be named Inspirations. It is intended that Inspirations will provide a high quality, bespoke holiday service for discerning clients. HC has decided that this new business unit will have its own mission statement of ‘delivering a high quality service for discerning travellers’. The new managing director of Inspirations has stated that it has an objective of achieving annual revenue of $100m by 2018. This would be approximately 25% of the total forecast revenue for HC that year, but it is expected to represent only about 5% of the total number of holidays sold by HC. The type of holidays offered by Inspirations is already provided by some of HC’s competitors.

Dilip Kharel, the new director of marketing of Inspirations, has stated that the internet should be increasingly used as the main source of marketing and selling the holidays, as ‘the days are almost gone when families visit a ‘high street’ travel agency to plan their holiday; it’s all done now from the comfort of the home’. He believes that potential customers of Inspirations will not want to visit high street travel agencies.

HC currently makes extensive use of traditional marketing techniques, sending out travel brochures containing all of its holidays to potential customers. However, as Dilip has recognised, ‘the problem is that we don’t even know if our customers bother opening these, or if they put them directly into the dustbin.’ These brochures are often produced months in advance, and may advertise holidays which are no longer available. Customers will not discover this until they visit one of the travel agents. The company currently does make some use of targeted emails, but it has been accused of sending spam mail in the past and mass mailing a weekly email of all current holiday offers to everyone registered on its database.

Dilip is keen to embrace the opportunities offered by electronic marketing and believes that Inspirations can benefit greatly by exploiting the principles of intelligence, individualisation, interactivity, integration and independence of location which are central to electronic marketing.

Inspirations will offer holidays in a wide variety of locations, including the Caribbean, Africa and Asia, and plan to offer ‘themed’ trips, such as gourmet food holidays and heritage trips. Different countries may have different requirements for visiting tourists, such as visa regulations. Inspirations does not own hotels or aircraft and therefore the majority of holidays offered will be provided by third-party suppliers, such as hotel and airline companies. This means that Inspirations can lack control over some elements such as passenger taxes. Inspirations will have representatives on site in all resorts to meet guests at airports and to address any issues they have with the holiday. However, the hotels and excursions will not be solely or exclusively offered to Inspirations guests. For example, there will be other guests at a hotel who have not booked through Inspirations.

Dilip is concerned about this. He feels that the company needs to be able to differentiate itself, either in the overall holiday experience itself or in the marketing of it, so that customers are more likely to book such holidays through Inspirations, rather than through a competitor, or indeed through booking with the hotel directly. He also recognises the importance of adopting an appropriate pricing strategy which meets the needs of the organisation (HC and Inspirations) and customers alike.

Required:

(a) Evaluate how the principles of intelligence, individualisation, interactivity, integration and independence of location could be exploited when marketing the new range of holidays to be offered by Inspirations. (15 marks)

Dilip Kharel recognises the importance of a pricing strategy which supports the overall corporate and business strategies of the organisation.

Required:

(b) Describe a strategic approach to establishing prices in the context of Inspirations. You should recognise both economic and non-economic factors in your approach. (10 marks)

-

Section A – This ONE question is compulsory and MUST be attempted

Introduction

QTP Co produces timber framed windows for builders’ merchants, property builders and property maintenance companies. It does not sell windows directly to the general public. Members of the general public (and small building companies) can buy QTP windows through the builders’ merchants supplied by QTP. These builders’ merchants supply a wide range of products for property maintenance and improvement. They are usually located in large warehouse premises on the outskirts of towns and cities.

There are three primary raw materials (or components) for the windows which QTP makes.

– Timber (wood) which it orders from timber suppliers. Worldwide demand for timber is increasing and timber prices are relatively high and supply of some of the specialist timber which QTP requires is often in short supply.

– Glass which it orders from specialist glass manufacturers.

– Fittings, such as bolts, latches, handles, etc which it sources from a number of small specialist producers.

QTP has a number of departments. This scenario considers just five of these departments and each of these departments is exactly aligned with activities of the value chain. They are:

– Inbound logistics and procurement

– Production

– Outbound logistics

– Marketing and sales

– Service

Production takes place on one dedicated production line where one machine (and supporting labour) undertakes all the tasks concerned with converting the components into the finished windows. There are no plans to buy a second machine or open up a second production line. Production takes place from 08.00 to 17.00 (nine hours). Although employees take breaks, these are organised so that the production line is always staffed. It is not possible, because of technical and environmental constraints, to extend the working day or organise a night shift. The company is effectively restricted to a nine-hour working day. Setting up and setting down of the machine has to take place within this nine-hour day.

Outbound logistics has a small fleet of vehicles which are used to deliver finished windows to the customer. Effective scheduling of this fleet is currently a problem and vehicle maintenance is becoming more expensive as the vehicles get older.

Standard and bespoke windows

The company offers both standard windows and bespoke windows.

Standard windows are made to a specification decided by QTP and they are produced to inventory. These windows are advertised in the company’s catalogue and on its website. Customer orders for these windows are supplied from inventory and next day delivery is promised. The production of these windows is based on sales forecasts made by the marketing and sales department. These forecasts are used by the inbound logistics and procurement department to place orders for the raw materials for the windows. Because relatively large orders for components are placed in advance, QTP usually obtains significant discounts on published component prices.

Bespoke windows are produced to a specification required by the customer, usually resulting from consultation and negotiation between the marketing and sales department and the customer. They are made to exactly fit the customer’s needs, in terms of timber type and quality, glass specification, window size and types of fitting. The marketing and sales department provides the customer with a proposed delivery date. A copy of the order, and the proposed delivery date, is also given to the production department, so that they can schedule the making of the windows and to inbound logistics and procurement so that they can order specific components for the windows.

At present, there is often a conflict between the production of standard and bespoke windows. It is essential that QTP achieves the promised delivery date for bespoke orders. To achieve this, it is often necessary for scheduled runs of standard windows to be postponed so that bespoke windows can be produced. This leads to less efficient use of the machine and labour (due to set up and set down time) and also to components for standard windows being held in inventory for longer than planned. Furthermore, component prices for bespoke orders are usually higher, reflecting smaller volumes and the need to fulfil tight deadlines. Bespoke window production and delivery to customers usually takes place as quickly as possible, to ensure that promised deadlines are met and inventory storage of finished windows minimised.

In the past, it was possible for bespoke orders to use common components bought in for standard windows. However, this led to continual disruption of the production of standard windows and now components for standard and bespoke orders are kept quite separate and are stored in different areas of the warehouse.

In general, the marketing and sales department prefers to make bespoke sales, rather than sales of the standard windows. They believe that bespoke windows provide exactly what the customer wants and this distinguishes QTP from its competitors who are more focused on selling standard windows. Unlike these competitors, the marketing and sales department at QTP contains staff who are experienced in window design and applications and customers value this. There is evidence that some important customers purchase their standard windows from QTP even though they could buy similar windows cheaper elsewhere, because they value QTP’s flexibility in supplying them with bespoke windows. The marketing and sales director claims that, ‘we have sales people who really understand windows and what customers want and need. We are not trying to sell them windows off-the-shelf, just because we have them in inventory.’

Furthermore marketing and sales staff claim that bespoke windows deliver higher revenue and higher profit to QTP than standard windows. However, this is challenged by the production manager who would prefer production to be focused on standard windows. Sales staff are currently rewarded on the basis of average revenue per window. At present, approximately 30% of QTP’s sales volume is for bespoke windows, but this share is increasing annually.

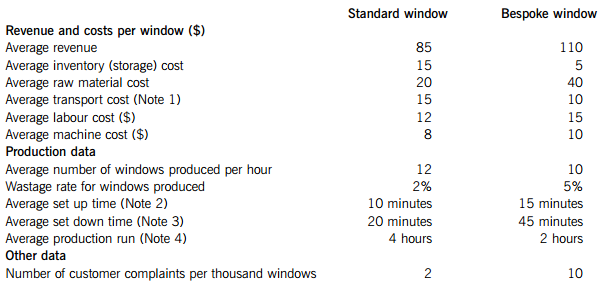

Table One shows selected data for the production of standard and bespoke windows.

Table One: Selected QTP data: standard window and bespoke window production

Note (1) Transport costs concern distribution costs of finished goods to customers. Costs of inbound components are borne by the supplier.

Note (2) Time taken to set up the machine for a single production run of windows to one specification.

Note (3) Time taken to set down the machine (resetting parameters, cleaning, etc) from a single production run of windows to one specification.

Note (4) Time of a single production run of windows to one specification.

Important: The machine is restricted to a nine-hour working day. Set up time and set down time must be within this nine-hour working day.

Management concerns

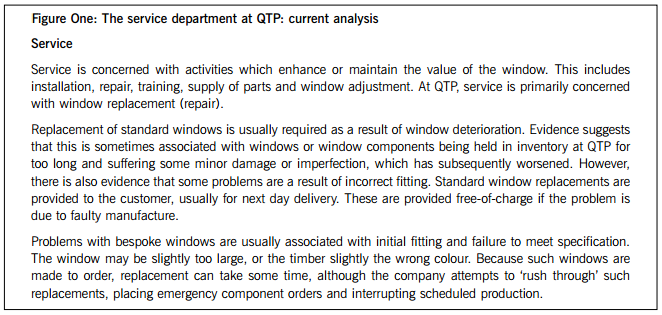

Senior management at QTP is exploring the possibility of moving the company to solely standard window production OR solely bespoke window production. They are also investigating issues in the five departments which are aligned to the activities of the value chain. They previously employed a business analyst who provided them with an analysis of the service department at QTP, documented in Appendix 1. Management has engaged you as her successor and they now require similar analyses for the remaining four departments.

Appendix 1: Analysis of service department in the value chain

Required:

QTP management would like you to prepare a briefing paper which:

(a) Analyses the current issues in the remaining four departments under consideration (inbound logistics and procurement, production, outbound logistics, marketing and sales), with appropriate reference to each department’s role in the value chain. Appendix 1 Figure One is representative of the approach required. (20 marks)

(b) Evaluates the financial case for EITHER producing and selling standard windows only OR producing and selling bespoke windows only. The evaluation should include both options and could include any comments you have on the limitation of the data given in Table One. However, you should assume that the data given in this table accurately reflects the current situation. (12 marks)

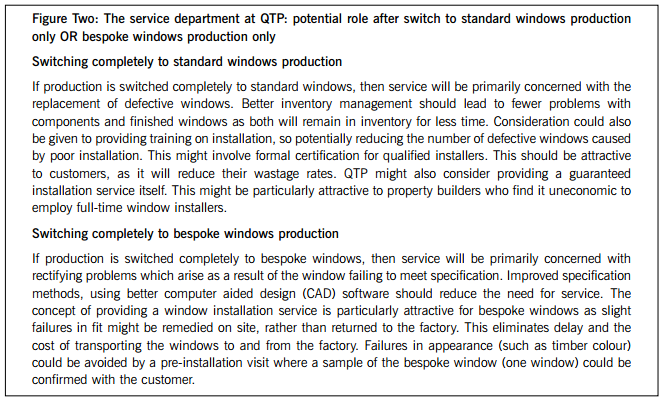

(c) Analyses how the company could restructure elements of each of the remaining four departments (and hence the value chain) in the future for EITHER a switch to only standard windows production OR a switch to only bespoke windows production. Appendix 1 Figure Two is representative of the approach required and it clearly shows that you should include BOTH options in your analysis. (14 marks)

Professional marks will be awarded in question 1 for the structure, tone, coherence and clarity of your briefing paper. (4 marks)